The COVID-19 pandemic and the difficult economic conditions that followed have increased the cost of doing business across the United States. Inflationary pressures have led to significant changes in the cost of goods and labor. To reduce the impact of these pressures, business leaders have looked for ways to reduce costs, often by reducing staff, decreasing production, or looking for other ways to improve efficiencies.

One area businesses should explore to improve efficiencies and reduce costs is accounts payable (AP) automation.

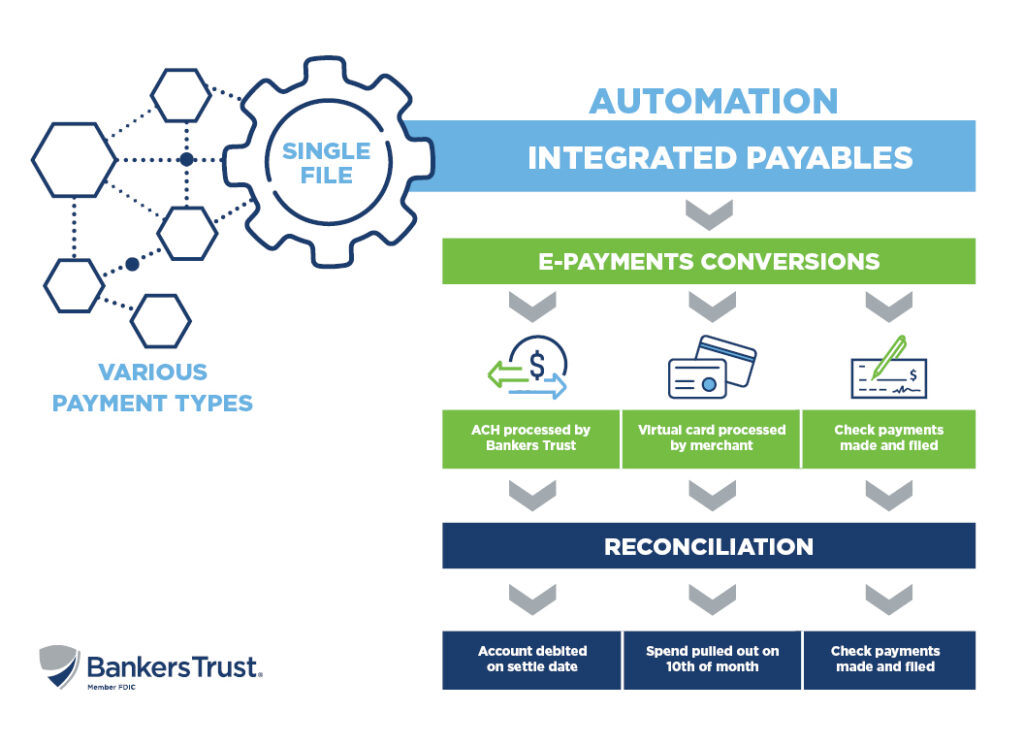

How AP Systems Work

An automated payables system consolidates a business’s payment generation process into a single file. Most businesses use checks, ACH, wires, and credit cards for accounts payables. Traditionally, each of these payment methods required a separate file to generate a payment, which required significant human intervention and other costs to carry out each day.

Through an automated system, all these files are consolidated into a single payment file. An artificial intelligence (AI) program reads this file, separates it into subsequent payment files and processes the files so all payees receive the correct payment type. This reduces room for human error and reduces labor costs.

Electronic Payment Options

While electronic payments have grown in popularity over the last two decades, many businesses still use checks for payments. However, this option comes at a high cost. According to the leading financial services company FIS, printing a check in-house costs most businesses $4.00 per check. This includes the cost of the paper, ink, printer, envelopes, stamps, and an employee’s time to manually process it. Automation service providers print hundreds of thousands of checks per day. This reduces the overall cost to produce a check by as much as 75%.

Additionally, an automated AP process can mimic a company’s existing payment approval process and include fraud mitigation reviews. These efficiencies reduce the time it takes to produce payments and allow companies to manage their payment process from anywhere.

Checks remain the payment method most preferred by fraudsters. The Association of Financial Professionals found that over 60% businesses surveyed in 2020 encountered some type of check fraud. ACH and virtual card payment methods came in at 19% and 3%, respectively. With these risks in mind, more businesses understand they must find alternatives to checks, and AP automation systems are an attractive option.

Additional Product and Service Options

To further encourage this transition, many AP automation system providers offer vendor data management. This is typically offered through a portal where vendors can manage their accounts, choose payment preferences and monitor incoming payments. Some providers also include ACH verification services within the portal, which allows the service provider to electronically verify the ownership of submitted account and routing numbers. This extra step helps reduce the likelihood of a payment being sent to a fraudulent account.

By taking ownership of vendor data management, the AP automation system provider eliminates the need for businesses to maintain account and routing numbers. Businesses can purge this data from servers, significantly reducing their liability if a data compromise were to occur.

Most AP automation systems also offer one-time use virtual card payments as another way to reduce paper checks. Unlike a typical virtual card generated through a purchasing-card system, automated AP systems generate a card number used for a single transaction. The transaction limit is set to the amount of the payment. Once the card is processed, the system deletes the card and prevents it from being used again.

Since these payments process as credit cards, they are subject to interchange fees, which are charged after the vendor processes the virtual card through their merchant terminal. The interchange fees are typically a small percentage of the entire transaction. Many automation system providers will share part of these fees with the payor, providing a new revenue stream to the business.

The Bottom Line

Manual AP processes remain costly, inefficient and prone to fraud. Through automation, a business can significantly reduce its cost, time spent generating payments and fraud exposure, and even earn additional revenue. These technologies help revolutionize AP processes and give team members more time to focus on activities that provide more benefit to the business.

If you found this article helpful, stay tuned for my next articles diving deeper into integrated payables and integrated receivables. If you would like to know how any of these solutions could benefit your business, please contact me or one of our Bankers Trust Treasury Sales Officers.

Equal Housing Lender. SBA Preferred Lender. NMLS #440379

Equal Housing Lender. SBA Preferred Lender. NMLS #440379