Millennials – those born between 1981 and 1996 – tend to get a bad rap for many things, such as being obsessed with social media, politically disengaged, and hesitant to marry and follow a traditional life path, just to name a few. One of the biggest concerns surrounding millennials is their financial situation.

According to a 2019 nationwide wealth survey by Charles Schwab, close to 75 percent of millennials live paycheck to paycheck, and less than half say they feel “financially stable.” Around 37 percent of millennials own homes, while close to half of baby boomers and gen Xers owned homes when they were the same age.

Why are millennials so financially behind?

Many factors have contributed to their financial instability, and they mostly stem from the economic climate around the time most millennials entered the workforce: the financial crisis of 2008, otherwise known as the Great Recession.

The financial crisis contributed to millennials’ financial struggles in two ways: their employment outlook and long-term debt.

Employment

Most millennials entered the workforce in the late 2000s, just in time for the financial crisis and a nation-wide hiring slow-down. Many baby boomers – the group of professionals working toward retirement – were hit hard by the economic crisis as well, causing them to postpone retirement. This means in addition to facing potential hiring freezes for new positions, existing positions were not opening up either, leaving many millennials desperate for any job, even one for which they’re overqualified.

Although unemployment rates have come down significantly since 2007, economists report wages have become stagnant while the cost of living has increased greatly, creating a new financial problem for millennials.

Debt

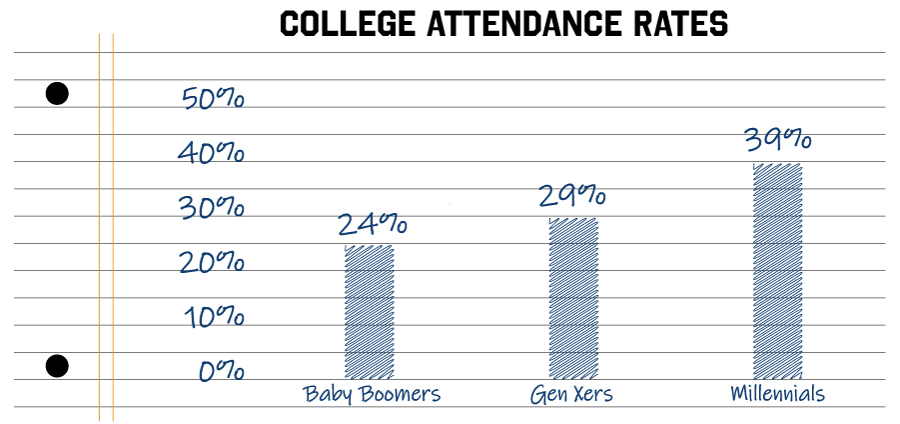

Millennials are the most educated generation in U.S. history. While about 24 percent of baby boomers and 29 percent of Gen Xers went to college, 39 percent of millennials earned a bachelor’s degree or higher. With the rise of tuition, this education came at a steep cost. The average millennial graduates from college with $33,000 in student debt. Faced with unemployment or a low-paying job, many millennials struggled to pay off these loans, and many even turned to other forms of borrowing, such as high-interest credit cards, to make ends meet.

High debt, stagnant wages and increasing living expenses have led many millennials to postpone – or forgo entirely – many life milestones, such as buying a home and starting a family.

So what can millennials do? Are they simply doomed?

Despite economic conditions leaving them financially behind, millennials are working hard to catch up. They’ve also developed a mindset crucial to helping them progress. Watching a recession unfold has inevitably made millennials a risk-averse generation. They are cautious with their finances, and they are known to vigorously research their options before making a purchasing decision. After all, millennials are digital natives! Naturally, they turn to social media and the internet to evaluate their options, and they don’t make spending decisions rashly.

Witnessing an economic recession has also instilled the importance of saving and budgeting among millennials. Contrary to popular opinion, most millennials are actually highly disciplined financial planners. A survey by Northwestern Mutual found that millennials are more likely than other generations to stick to their financial plan, with nearly 75 percent sticking to their monthly budgets!

Recent economic improvements are working in millennials’ favor as well. Unemployment rates are at a historic low, and even the youngest baby boomers are leaving the workforce, opening up senior level positions for millennials. It’s safe to say things may be looking up for millennials.

In addition to avoiding risky financial choices and moving up in the workforce, there are a few other moves millennials should consider to improve their financial situation:

1. Live in a smaller, inland city

Issues of home affordability and employment tend to be highly concentrated on the coasts. Growing cities in the Midwest and other inland areas offer a more stable job market, more affordable housing, shorter commute times, lower crime rates and better public education.

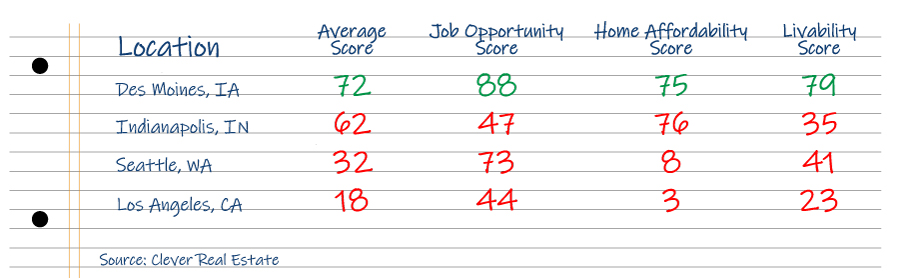

A 2019 study by Clever Real Estate looked at the 100 most populated cities in the U.S. and determined the “best” and “worst” places for millennials to live. Each city was assigned a score ranging from one to a 100, with one being very hard to live in and 100 being a great place to live. Scores are based on a few key components, such as job opportunity, home affordability and livability (i.e. commute times, crime rates and education levels). Take a look at four cities – Des Moines, Indianapolis, Seattle and Los Angeles – whose scores are scattered throughout the spectrum:

As you can see, the two coastal cities, Seattle and Los Angeles, have much lower overall scores than the two inland cities, Des Moines and Indianapolis. While Seattle may have a high “job opportunity” score due to the area’s recent tech boom, its housing market hasn’t caught up, leaving young professionals paying high prices for rent, postponing homeownership, and possibly even living in an outlying city despite a long commute to work. Los Angeles’s home affordability score is even lower than Seattle’s, and it does not offer a positive job outlook.

Des Moines and Indianapolis, on the other hand, score well above 50 – the “average” mark. Des Moines was rated the second best place for millennials to live based on its healthy job market, affordable housing prices, short commute times and low crime rates.

There are many quickly growing, vibrant, under-the-radar cities in the Midwest that are attractive to millennials. Even millennials who moved away from inland cities are making their way back! Gen Zers may want to take note of this trend. Before you set out to fulfill your big city dreams, consider the financial opportunities of keeping your job search inland.

2. Make additional payments toward student loans

Most millennials cite student debt as their biggest burden and roadblock. One of the fastest ways to pay off student loans is to make extra payments toward your remaining principal balance. There is no penalty for prepaying your student loans, so be sure to take advantage of this benefit whenever you have extra funds.

It’s important to remember that lenders are required to apply your payments first to the interest and fees accrued since your last payment, which accrue daily, and then apply remaining payment toward your principal. Extra payments will follow this same structure. Talk to your lender and set up specific instructions to ensure the maximum amount of your extra payments goes toward principal.

Check out this article for additional strategies for paying off student loans.

3. Save for retirement

Living with student debt and little savings, many millennials choose to postpone saving for retirement. However, the longer you wait to begin making contributions to a retirement plan, the larger your contribution will need to be in order to catch up. You’ll also earn less interest over your account’s lifetime.

Take advantage of employer matches and consider making automatic monthly contributions that are deducted from your paycheck. When you automatically contribute to your 401(k), it’s money that you never see and therefore is easier to live without.

The rise of the “experience” economy

There’s no doubt millennials have made and will continue to make a major economic impact. One major way they will continue to remold the economy is by putting their money behind “experiences” over tangible products. Seventy-eight percent of millennials claim they prefer spending discretionary money on events and travel over buying tangible products.

This shift to an experience-centric economy also stems from the devastating financial crisis. Witnessing the value of ownership plummet has made many millennials desire purchases that cannot lose value. While many millennials still strive to build equity of some kind, their spending habits revolve around an experience and longer-lasting benefits.

Millennials are the largest living generation, and they’re entering their prime spending years. How will this affect the economy? How do the spending habits of generation Z compare, and are they set to deal with the same financial issues as millennials? Stay tuned as we tackle these topics!

Equal Housing Lender. SBA Preferred Lender. NMLS #440379

Equal Housing Lender. SBA Preferred Lender. NMLS #440379