Just 20 years ago, a “real-time payment” meant handing someone cash, and many business’s main method of paying their vendors was writing checks, sending them in the mail, and waiting several days for them to process. Today, payments are cleared much faster when using methods such as Same-Day ACH.

Despite Same-Day ACH – which itself was implemented and rolled out by NACHA, The Electronic Payments Association, a few years ago – significantly increasing the speed of payments, demands for faster processing still linger. Driving the demand for faster payments – cleared in minutes or even seconds – are consumers, technological innovation, and businesses themselves looking for more efficient ways to send and receive payments. As a result, The Clearing House (TCH) introduced a real-time payments network (RTP), which represents the first major upgrade in electronic payments since the Automated Clearing House (ACH) was created 40 years ago and Check 21 launched in 2001.

What is a real-time payment?

A real-time payment is a payment that is transferred immediately and cleared within minutes. Unlike Same-Day ACH payments, which are processed in batches and require payments to be submitted within a certain window of time, real-time payments are settled instantly.

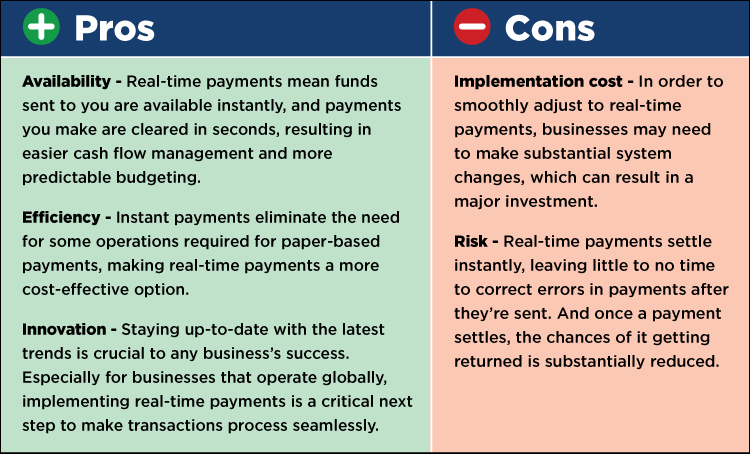

What are the advantages and disadvantages of real-time payments?

Like with any new development, there are benefits as well as potential disadvantages to keep in mind. Here’s a breakdown of each:

Where does the United States stand in adoption of real-time payments?

Adopting a real-time payments strategy broadly in the United States will require all of its key players throughout the private and public sector to agree on a comprehensive approach to adoption and implementation. In many other countries across the globe, adoption is mandated by the government or the central bank, making the transition easier and straightforward. Therefore, we are seeing higher adoption rates outside of the United States.

What’s next for real-time payments?

Many private and public sector players in the United States are working both collaboratively and independently to create an infrastructure and put a process in place that would in return create sustainability and allow for evolution of systems to address evolving security threats and aid in greater adoption of faster payments.

The Clearing House, which owns an RTP network, creates additional pressure for the Federal Reserve, who is still trying to decide whether the Fed should play a role in creating a payment rail that would allow for instantaneous settlement of payments. The RTP network provided by The Clearing House is live now and any financial institution can become a participant.

Equal Housing Lender. SBA Preferred Lender. NMLS #440379

Equal Housing Lender. SBA Preferred Lender. NMLS #440379