Saving money is a prudent practice, and it’s never too late to start putting money away for future needs, such as costly emergencies, expenses, vacations and retirement. Most people start by tucking money away from each paycheck into a bank savings account. In a savings account, money can continue to grow because it’s held separately from the account in which monthly bills are paid and is harder to access electronically. Money held in a bank savings account also earns interest, another reason to keep it separate from a checking account that typically pays no interest. Having money in savings can give you peace of mind knowing you have extra money on hand when a financial need should arise.

Interest earned on savings balances can add up to extra money in your pocket over time, but a savings account pays the lowest interest rate when considering various savings options. When you’ve successfully accumulated more money in savings than what you will need for future emergencies or expenses, it may be time to look at investing in a savings option that pays more interest. One option that can help you do this is a product called a Certificate of Deposit, or CD for short.

A CD is an investment product you can open at a bank. Most CDs are opened with a single sum, for example $1,000, rather than making regular deposits. However, there are some CDs for retirement that will accept smaller, ongoing deposits. CDs are purchased for a specific “term,” such as 12-months, and the idea is that you will not have access to your money for that period of time. You choose the term of the CD before investing, which usually ranges anywhere from 90 days to 5 years. If you need to use the money prior to the end of the term, a penalty fee is charged on the amount withdrawn. The penalty can be significant, and you can lose principal, so be sure to deposit money you will likely not need to access for the duration of the CD’s term.

Benefits of Opening a CD

The biggest advantage is that pledging your money to a CD for a specific period of time means a higher rate of interest than a savings account. The difference can be significant, making it worthwhile to let the money sit untouched.

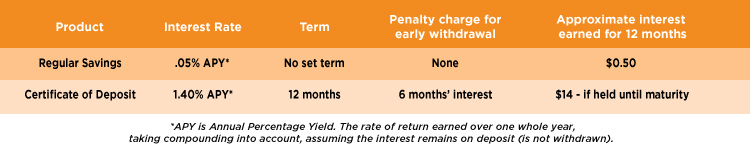

Using rates in the current interest rate environment, the illustration below shows the differences between saving $1,000 in a CD and a regular savings account. The larger the balance in the account, the more interest you will have at the end of the year. This simple illustration assumes there is no money added or withdrawn from the $1,000 investment and there is no compounding of interest during the year.

It is recommended that you have a blend of investment vehicles in your “portfolio,” which means you should have some that you can draw from if needed (savings) and some available for future use (CDs). This enables you to have what’s necessary for your upcoming needs and also earn a higher interest rate on money you won’t need for a while. Both types of accounts are insured by the FDIC, a federal agency that insures deposits in member banks up to $250,000.

Most banks offer several options for CDs and savings accounts. A banker can guide you through the process of determining how much and how long to invest. By asking questions about your budget, spending and future needs, your banker can advise you in implementing a savings plan that’s right for you. The important thing is to get started as soon as possible! If you are already a seasoned saver, it makes sense to consider adding a CD to your plan to help you reach your financial goals sooner.

Equal Housing Lender. SBA Preferred Lender. NMLS #440379

Equal Housing Lender. SBA Preferred Lender. NMLS #440379