In the process of buying a home, you’re likely to encounter dozens of mortgage terms that are unfamiliar, especially if you’re a first-time home buyer. If you’re looking to purchase a home or plan to in the future, brush up on your mortgage terminology with this glossary to help you navigate any situation you may encounter.

Adjustable Rate Mortgage (ARM) – A mortgage loan or deed of trust which allows the lender to periodically adjust the interest rate in accordance with a specified index.

Amortization – The paying off of debt in regular installments over a period of time.

Appraiser – One who is trained and educated in the methods of determining the value of property (appraised value). You will pay a fee for an appraisal report containing an opinion as to the value of your property and the reasoning leading to this opinion. The appraisal report is required to process a loan request and the fee is included in your closing costs.

APR (Annual Percentage Rate) – Loans or credit agreements can vary in terms of interest-rate structure, transaction fees, late penalties and other factors. A standardized computation such as the APR provides borrowers with a bottom-line number they can easily compare to rates charged by other potential lenders.

Balloon Mortgage – A balloon payment is due on a mortgage that usually offers a low monthly payment for an initial period of time. After the period of time elapses, the full balance must be paid by the borrower, or the amount must be refinanced. The large sum payable at the end of the loan term is called the “balloon payment.”

Bridge Loan – A short-term, interim loan to help bridge the time between a borrower’s sale of his current home, and the purchase of a new home. If the new home purchase will close before the borrower reaps the proceeds from the sale of their current home, they may require a Bridge Loan to use for down payment on the new purchase. The Bridge Loan requires a one-time payment, due upon the sale of the current home and the realization of those proceeds.

Closing Disclosure – A Closing Disclosure is a five-page form that provides final details about the mortgage loan you have selected. It includes the loan terms, your projected monthly payments, and how much you will pay in fees and other costs to get your mortgage (closing costs). This disclosure is provided to you at least three business days before you close on the mortgage loan. This three-day window allows you time to compare your final terms and costs to those estimated in the Loan Estimate that you previously received from the lender. The three days also gives you time to ask your lender any questions before you go to the closing table.

Construction Loan – A short-term, interim loan for financing the cost of construction. The lender advances funds to the builder at periodic intervals, as work progresses. Typically, the construction loan is taken out by the Builder, but a buyer can also carry the construction loan. Once the project is completed, the loan is then refinanced as a long-term loan.

Conventional Loan – A private sector loan which is not guaranteed or insured by the US Government.

Credit Report Fee – This fee covers the cost of a credit report, which shows your credit history. The lender uses the information in a credit report to assess your credit worthiness.

Default – The inability to pay monthly mortgage payments in a timely manner, or to otherwise meet the mortgage terms.

Delinquency – Failure of a borrower to make timely mortgage payments under a loan agreement.

Down Payment – The portion of a home’s purchase price that is paid in cash and is not part of the mortgage loan.

Earnest Money Deposit – Money you will pay up front on the transaction to exhibit your sincerity about purchasing the home. You will receive credit for this up-front money at the time of closing if the offer is accepted, or have it returned to you if the offer is rejected. You may forfeit your earnest money deposit if you do not follow through with the deal.

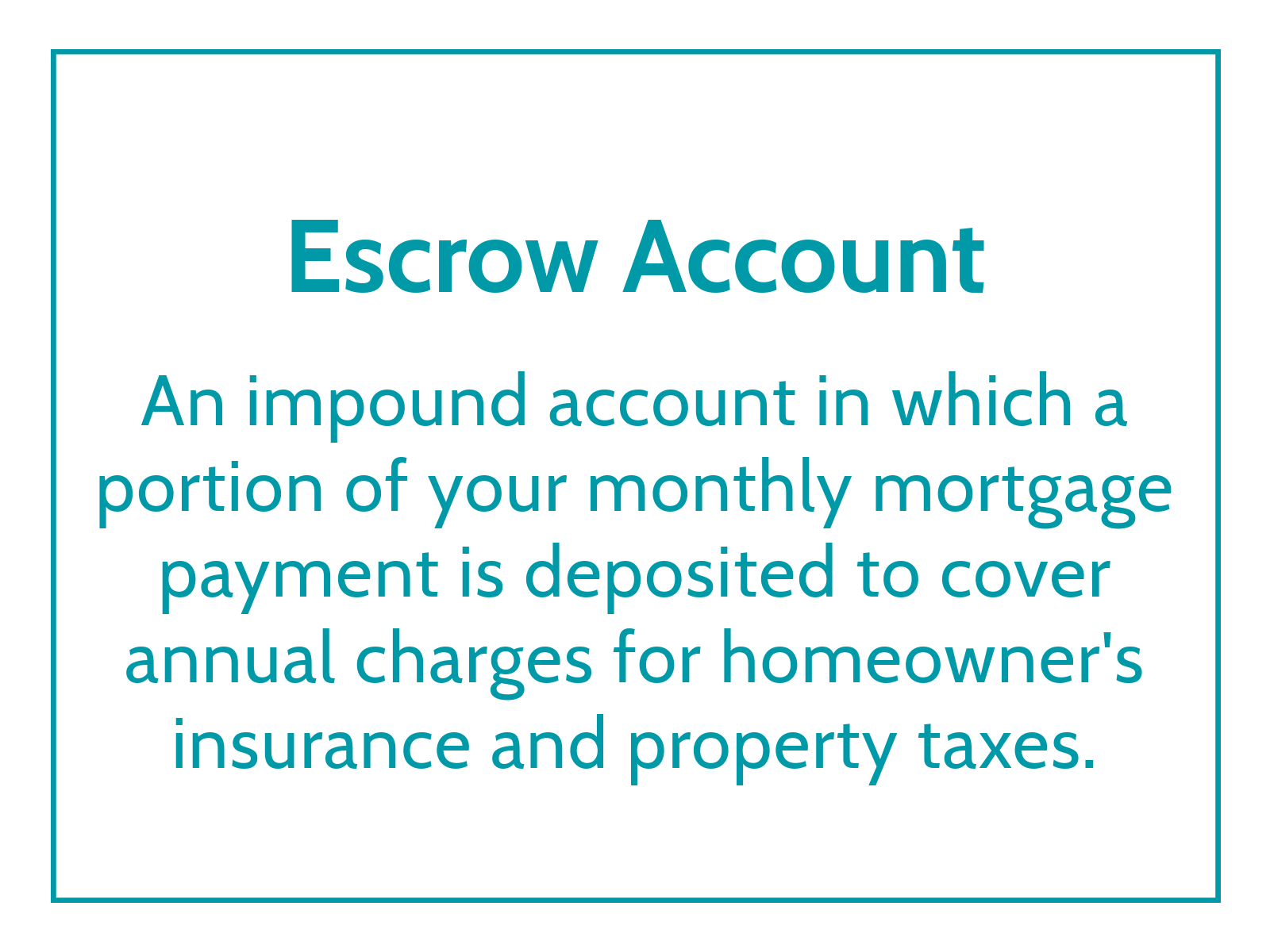

Escrow Account – An impound account in which a portion of your monthly mortgage payment is deposited to cover annual charges for homeowner’s insurance and property taxes.

Escrow Agent – A person or entity holding documents and funds in a transfer of real property, acting for both parties pursuant to instructions. Typically, the agent is a person (often an attorney), escrow company or title company, depending on local practices.

FHA (Federal Housing Administration) Financing – A Federally-insured loan program offered by the Government to FHA-approved lenders, such as Bankers Trust. When the Federal Housing Administration was established in 1934, it was intended to stimulate the housing industry. By providing insurance to lenders, the idea was that more people would be able to qualify for mortgages, and therefore, purchase a home.

Fixed Rate Mortgage – A mortgage with an interest rate that does not change over the life of the loan, and as a result, monthly payments for principal & interest do not change.

Flood Certification Fee – A fee for the assessment of your property to determine if it is located in a flood prone area.

Foreclosure – A legal process in which mortgaged property is sold to pay the loan of the defaulting borrowers.

FSBO – For Sale By Owner

Government Recording and Transfer Charges – Fees for legally recording your Deed and Mortgage. These fees may be paid by you or by the seller, depending upon the terms of the sales agreement.

Home Equity Line of Credit (HELOC) – A line of credit extended to a homeowner that uses the borrower’s home as collateral. Once a maximum loan balance is established, the homeowner may draw on the line of credit at his or her discretion. Interest is charged on a predetermined variable rate, which is usually based on prevailing prime rates.

Home Inspection – An inspection of the mechanical, electrical, and structural aspects of your home. A fee is charged for this inspection, and the inspector will provide you a written report evaluating the condition of the home. Typically, this fee is paid by the seller, but that would be negotiated at the time of the offer. The inspection is considered protection for the buyer, but is not required for financing.

Homeowner’s Insurance or Home Hazard Insurance – An insurance policy that protects your home and your possessions inside, from serious loss, such as theft or fire. This insurance is usually required by all lenders to protect their investment and must be obtained before closing on your loan.

Interest – A fee charged by the lender for the use of its money.

Interest-Only Payments – An interest-only payment plan allows you to pay only the interest due for a specific number of years; typically on an Adjustable Rate mortgage. This allows you to have smaller payments for a period of time. After that, your monthly payments will increase, even if the interest rate stays the same, because you must start paying back the principal, as well as the interest each month.

Interest Rate – The charge by the lender for borrowing money, expressed as a percentage.

Lender Inspection Fees – This charge covers inspections, often of newly constructed housing, made by employees of your lender, or by an outside inspector.

Loan Estimate – A Loan Estimate is a three-page form that you receive after applying for a mortgage. The form provides you with important information, including the estimated interest rate, monthly payment, and total closing costs for the loan. The Loan Estimate also gives you information about the estimated costs of taxes and insurance, and how the interest rate and payments may change in the future. In addition, the form indicates if the loan has special features that you will want to be aware of, like penalties for paying off the loan early (a prepayment penalty) or increases to the mortgage loan balance even if payments are made on time (negative amortization). If your loan has a negative amortization feature, it appears in the description of the loan product.

A Loan Estimate is required to provide a good faith estimate of closing costs that are expected to remain consistent with certain final closing costs. Some closing costs cannot increase from what is provided on the Loan Estimate, while other closing costs may have limited increases that do not exceed the sum of the original disclosed cost by more than 10 percent. This rule protects you from costs skyrocketing after the Loan Estimate has been provided. Should important information change, a revised Loan Estimate is required to be provided to you. A revised Loan Estimate may be required whenever, (1) Changed circumstances affect the settlement charges, (2) Changed circumstances affect your eligibility for the loan applied for, or (3) You request revision to the credit terms or settlement that results in an estimated charge to increase. If your Loan Estimate is revised, you should carefully review it to determine what changed.

Loan-to-Value (LTV) Ratio – A percentage calculated by dividing the amount to be borrowed by the price or appraised value of the home to be purchased (whichever is less). The loan-to-value ratio is used to qualify borrowers for a mortgage, and the higher the LTV, the tighter the qualification guidelines for certain mortgage programs become. Low loan-to-value ratios are considered below 80%, and carry lower rates, since these borrowers are considered lower risk.

Mortgage – The transfer of an interest in property to a lender as a security for a debt. This interest may be transferred with a deed of trust in some states.

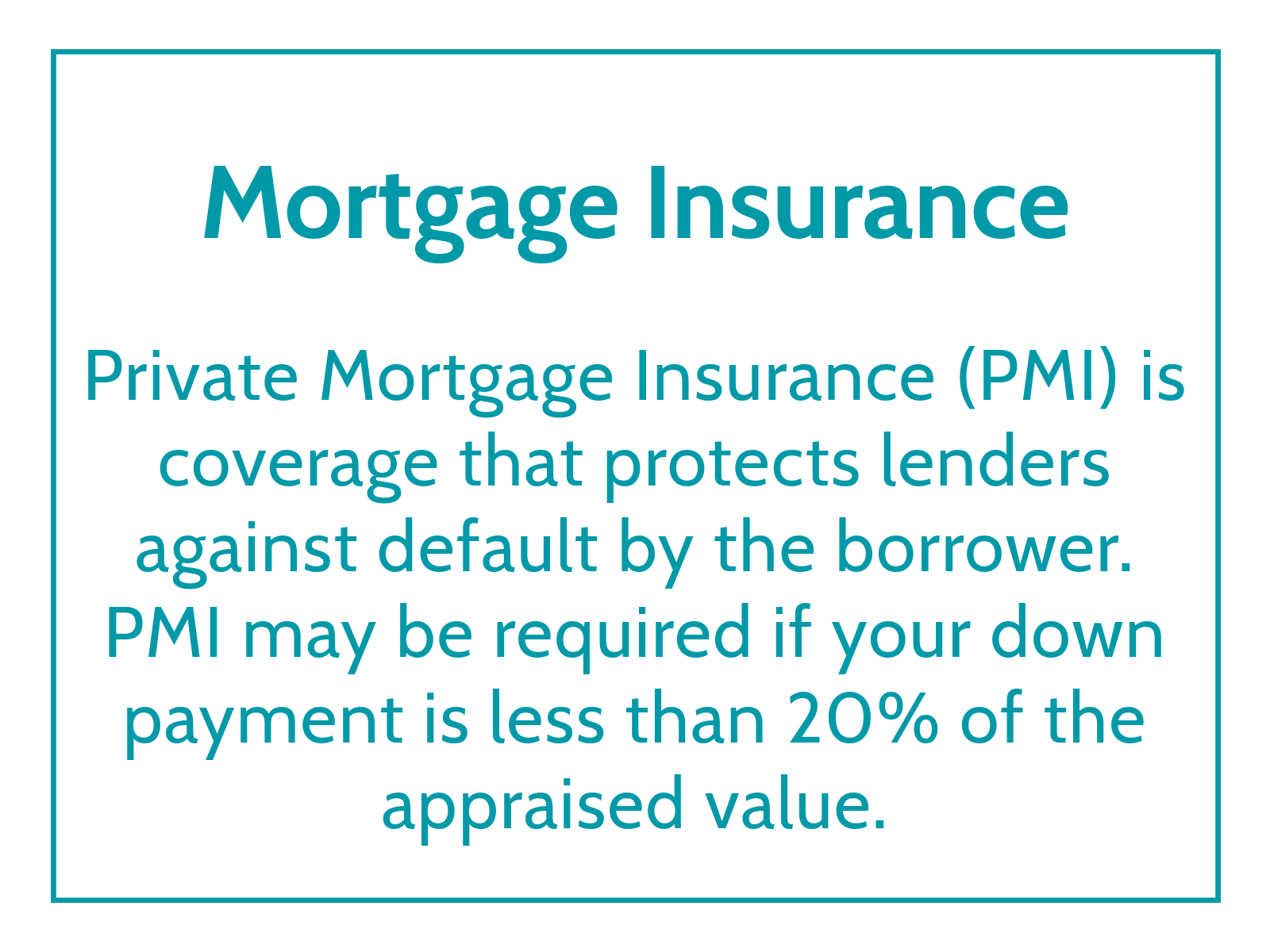

Mortgage Insurance – If your down payment on a home is less than 20% of the appraised value or sale price, your lender may require you to pay mortgage insurance. Also known as Private Mortgage Insurance (PMI). The coverage protects lenders against default by the borrower.

Origination Fee – A fee charged to the borrower to cover various origination services when making

a mortgage loan. This fee is usually a percentage of the face value of the loan.

Origination Services – Any service involved in the creation of a mortgage loan, including but not limited to, the taking of the loan application, loan processing, and the underwriting and funding of the loan, and the processing and administrative services required to perform these functions.

Payment Shock – A scenario in which monthly mortgage payments on an Adjustable Rate Mortgage (ARM) rise so high during future adjustments that the borrower may not be able to afford the payments.

Pest Inspection – An inspection for termites or other pest infestations of your home. This inspection is frequently required by your lender.

PITI (Principal, Interest, Taxes and Insurance) – The four elements of a monthly mortgage payment. Payments of principal & interest go directly towards repaying the loan while the portion that covers taxes and insurance goes into an escrow account to cover the fees when they are due.

Point(s) – Amount of money paid to reduce the interest rate on a loan. This is a negotiable fee.

Pre-Paid Items – Lenders often require the prepayment of items such as insurance premiums for private mortgage insurance, homeowner’s insurance, and real estate taxes.

Prepayment Penalty – A fee charged if the mortgage loan is paid before the scheduled due date. Bankers Trust offers NO prepayment penalty loans.

Recording and Transfer Charges – These charges include fees paid to the local government for filing official records of a real-estate transaction.

Sales Agreement – The contract signed by a buyer and the seller, stating the terms and conditions under which a property will be sold. It may also be called an “Agreement of Sale” or “Purchase Contract.” This agreement protects both you and the seller. Your agreement could allow the purchase to be cancelled if you cannot obtain mortgage financing.

Septic System Inspections – With very few exceptions, houses and buildings using septic systems must pass an inspection. The law is designed to ensure septic systems have both a tank and a functioning leach field, sand filter or other treatment device. Systems that do not have these features, must be upgraded when ownership transfers.

Settlement – The time at which the property is formally sold and transferred from the seller to the buyer. It is at this time that the borrower takes on the loan obligation, pays all closing costs and receives title from the seller.

Settlement/Closing Agent – The person who handles the real estate transaction when you buy or sell a home. It may be an attorney or title agent, but at Bankers Trust we act as the Settlement Agent for our buyers in the area. Loans completed outside of our immediate area use the services of another Settlement Agent. The agent will oversee all legal documents, fee payments, and other details of transferring the property to ensure that the conditions of the contract have been met and appropriate real estate taxes have been paid.

Settlement Costs/Closing Costs – The customary costs above and beyond the sales price of the property that must be paid to cover the transfer of ownership at closing. These costs generally vary by geographic location and are typically detailed to the borrower at the time the Loan Estimate is given. The costs include all third party fees that must be paid to process the loan. As a buyer, you can negotiate which settlement costs you will pay and which (if any) will be paid by the seller.

Short Sale – Any sale of real estate that generates proceeds that are less than the amount owed on the property. A real estate short sale occurs when the lender and borrower decide that selling the property and absorbing a moderate loss is preferable to having the borrower default on the loan. It is therefore an alternative to foreclosure.

Survey Fee – A fee for obtaining a drawing of your property, showing the location of the lot, any structures, and any encroachments. The survey fee is usually paid by the borrower.

Tax Certificate – Official proof of payment of taxes due provided at the time of transfer of property title by the state or local government.

Tax Service Fee – This fee covers the cost of your lender engaging a third party to monitor and handle the payment of your property tax bills. This is done to ensure that your tax payments are made on time and to prevent tax liens from occurring.

Tax Transcripts – A computer print-out of the information on your past tax return, rather than an exact copy of the full return. Ordering tax transcripts is a part of the loan process and included in your closing costs.

Title Insurance – Insurance that protects your lender against any title dispute that may arise over your property. Through a title search, the lender verifies who the actual property owners are and whether the property is free of liens. The title search company then issues title insurance which protects the title of the property against any unpaid mortgages and judgments. In case a claim is made against the property, the title insurance provides legal protection and pays for court fees and related costs. You may also purchase Owner’s title insurance, which protects you as the borrower.

Title Service Fees – Title service fees include charges for title search and title insurance, if required. This fee also includes the services of a title or settlement agent.

Equal Housing Lender. SBA Preferred Lender. NMLS #440379

Equal Housing Lender. SBA Preferred Lender. NMLS #440379