A simple way to prevent unauthorized access to your credit is to freeze your credit. This includes individuals trying to steal your identity and take credit out in your name and even companies placing inquiries on your report without your permission. Let’s go through when, how and why you would freeze your credit.

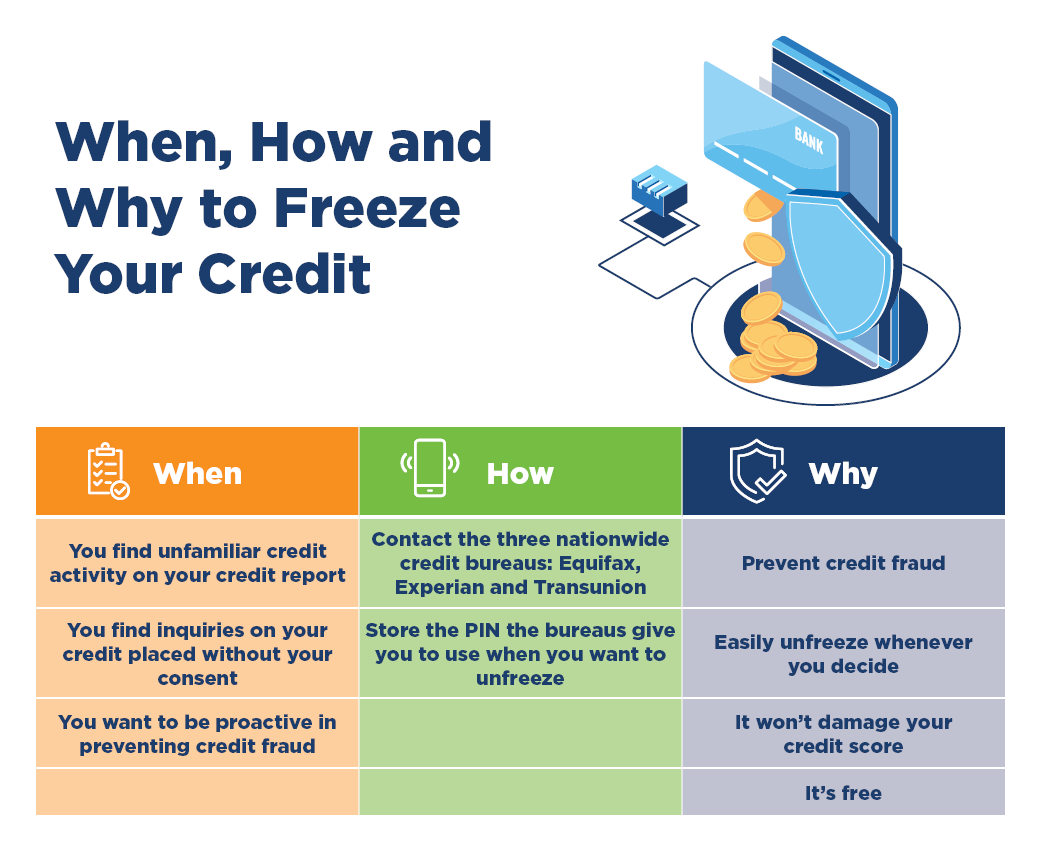

When should I consider freezing my credit?

The most common reason people freeze their credit is because they believe they are a victim of identity theft. Since placing a freeze on your credit – also known as a security freeze – will restrict access to your credit report, it makes it harder for fraudsters to access your information and open accounts in your name.

Other common reasons to freeze credit include finding inquiries placed by companies you didn’t give permission, finding new credit accounts opened that you don’t remember opening or losing your wallet and other important personal documents.

However, suspecting fraudulent activity isn’t the only reason you may decide to freeze your credit. Some individuals who don’t plan on needing credit anytime soon may put a freeze on their credit to proactively prevent suspicious activity on their account.

How do I freeze my credit?

To freeze your credit, you’ll need to call each of the three nationwide credit bureaus: Equifax, Experian and Transunion. Once the freeze has been placed, you’ll receive a PIN or password that you will need to know when you unfreeze your credit, which you can do online or by phone.

As of September of 2018, credit freezes and unfreezes are free under federal law.

Why should I freeze my credit?

Freezing your credit is a free and simple process that involves a couple of phone calls and can help prevent credit fraud.

Credit freezes are also easy to lift either temporarily or indefinitely. If you need to give someone access to your credit, simply call the three credit bureaus you placed a freeze with and provide your unique PIN and other personal information. You can also complete this process online by visiting the credit bureaus’ websites.

Freezing your credit will not harm your credit score, and it will not prevent you from receiving your free annual credit report. It also won’t prevent you from using existing open credit lines, only from opening new ones.

Better safe than sorry

Even if you decide not to freeze your credit, you may consider hiring a credit monitoring service. This ensures you receive notifications for all activity on your account, including new accounts opened, inquiries placed on your account, loans paid off, address changes, your credit score increasing or dropping, and even if you’re using a higher than usual percent of credit available to you. This ensures you’ll be aware of any suspicious activity on your account and can act quickly with an extra layer of security, such as a credit freeze!

Equal Housing Lender. SBA Preferred Lender. NMLS #440379

Equal Housing Lender. SBA Preferred Lender. NMLS #440379