With the spring season right around the corner, many homeowners are itching to renovate and improve their home. Whether you’re looking to put in that backyard pool you’ve always dreamed of, finally finish your basement or just replace your old furnace, a home equity loan or a home equity line of credit (HELOC) can help you kick off your big spring projects.

Home improvement is a great reason to use home equity. One benefit is that it’s considered an investment in your property. Any improvements or repairs you make today will likely increase the value of your home tomorrow.

Home equity loan versus HELOC

The amount of money you borrow is secured by the equity you have in your home, so the amount you’re able to borrow depends on how much you currently have paid off on your home. If you are eligible to borrow against the equity in your home, you have two options. You can either take out a fixed rate installment loan, also known as a home equity loan, or you can open a home equity line of credit (HELOC).

Home equity loans allow you to receive the entire sum you borrow up front and then pay that amount back in fixed monthly payments. The interest rate for home equity installment loans are fixed.

In contrast, a HELOC is a form of revolving credit, which means you borrow money as you go and only pay interest on the amount you use. The interest rate you pay on a HELOC depends on the prime rate, so it may increase or decrease over the term of the HELOC.

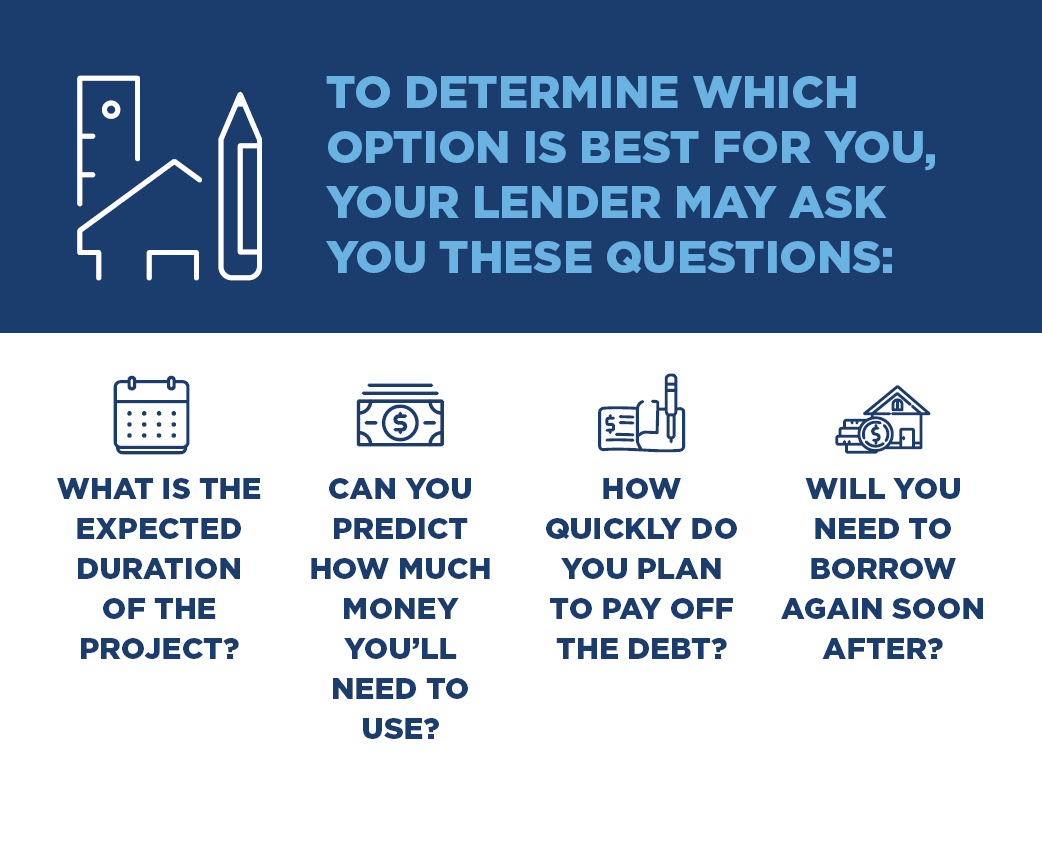

If you’re expecting your home improvement project to take a long time, and you’re unsure exactly how much money you’ll need to borrow in order to complete it, a HELOC may be a better fit for you, as it allows you to only pay interest on what you end up using.

If you know exactly how much you’ll need to borrow and expect to be able to pay it off quickly, and you don’t plan on needing to borrow again soon after, a fixed rate installment loan may be a better fit for your situation.

Whether or not you’ll need to borrow again soon after may be a determining factor in choosing between a loan and a line of credit. With a home equity loan, you’ll need to reapply for any subsequent loans and likely pay closing costs again. Since a HELOC is a form of revolving credit, it’s usually available to you for several years.

Another common deciding factor for people choosing between a home equity loan and line of credit is the current state of market rates. When rates are low, lines of credit tend to be more popular. When rates are rising, people tend to gravitate towards the predictability of a fixed-rate loan. However, neither is a one size fits all product, so you’ll need to consult your lender to determine which is a better fit for you.

Learn more about how Bankers Trust can help you make the most of the equity you have in your home by contacting me below or by browsing Bankers Trust’s loan products.

Equal Housing Lender. SBA Preferred Lender. NMLS #440379

Equal Housing Lender. SBA Preferred Lender. NMLS #440379