The subject of health care costs is something we hear about in the news on a weekly basis. There are many options when it comes to health insurance and it can be confusing when we try to compare what is available. One option is a health savings account (HSA). Let’s take a closer look at what an HSA is and how it works.

What is an HSA?

An HSA is a tax-favored consumer savings account for individuals to pay for qualified health care expenses.

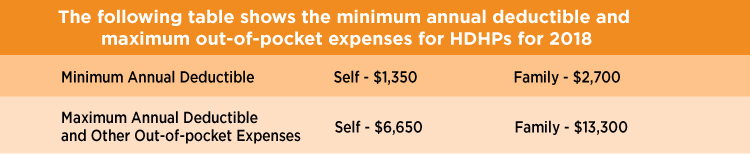

When researching ways to save money on health insurance premiums, a high deductible health plan (HDHP) is often recommended as a way to balance rising health care costs. HDHP deductible limits are higher than other health plan options, saving you big money on the cost of health insurance. The HDHP must meet specific IRS established minimum annual deductible and maximum out-of-pocket expense limits to qualify as an HDHP (see chart).

With the HDHP, you pay for medical expenses out-of-pocket up to the amount of your annual deductible for either a self or family coverage plan. After the deductible is met, the insurance plan coverage will pay for medical expenses. An HDHP may provide preventative care benefits without meeting the deductible, which can include annual physicals, immunizations, screenings, routine well-child care, and other health programs. Once you have an HDHP established, you’re able to use an HSA to pay or reimburse you for certain medical expenses.

How does an HSA work?

HSAs have two components: funds that are put in (contributions), and funds that can be taken out to use (distributions). Let’s look at each in more detail:

Contributions: An HSA can be opened at a bank and offers tax benefits for the money you set aside to pay out-of-pocket medical expenses up to the HDHP annual deductible. Contributions are made to the HSA at your discretion, up to the annual contribution limit in 2018 of $3,450 for self-only coverage or $6,900 for family coverage, and must be made by the tax return deadline for the previous year. Those over age 55 can contribute an additional $1,000 per year.

Contributions made to the HSA are excluded from gross income, and anyone can make contributions to the HSA on your behalf, such as a parent or spouse. HSA balances not used are carried over each year and the earnings are tax-deferred.

Distributions: An HSA belongs to the owner, so it can be withdrawn at any time; however, withdrawals are only tax free if used for qualified medical, dental and vision care expenses. If the HSA isn’t needed for medical expenses, the accumulated balance can be used long into retirement. If used for other purposes before age 65, there is a 20% IRS penalty and it’s taxed as normal income. Distributions due to death or disability are not penalized.

Your bank will send you the appropriate tax form(s) after the end of the year so all deposits and withdrawals can be reported. It’s important to talk with a tax professional regarding taxation of an HSA.

Who can qualify for an HSA?

If you want to save money in healthcare expenses using a tax-advantaged HSA, you must meet four qualifications:

- We discussed the requirement of having an HDHP, and you must be covered by the plan on the first day of the month you open the HSA

- You can’t be covered by another health plan (with certain exceptions)

- You can’t be enrolled in Medicare

- You can’t be eligible to be claimed as a dependent on another person’s tax return.

Employer Plans

Many companies offer their employees an HDHP/HSA health care option. Employers usually opt to make contributions to your HSA by direct deposit, and the contributions you and your employer make are tax deductible to you. It’s important to track what you are contributing, in addition to what your employer deposits, to ensure the total doesn’t exceed the annual contribution limit. One of the great things about an HSA is that it’s portable and stays with you if you change employers or leave the workforce.

Let’s Recap the Benefits of HSAs

- Using an HDHP with lower monthly premiums allows you to set aside money for health expenses in a tax-favored HSA.

- An HSA is a financially beneficial and convenient vehicle to pay for medical expenses for yourself and your family.

- Most financial institutions that provide HSAs offer competitive interest rates in various investment vehicles and provide online access for ease in managing expenses.

- Because there is no deadline to use the funds annually, accumulated balances carry over each year creating retirement savings for your future.

Equal Housing Lender. SBA Preferred Lender. NMLS #440379

Equal Housing Lender. SBA Preferred Lender. NMLS #440379