We’ve all thought about putting money aside for a rainy day. Regrettably, understanding the best way to do so isn’t as simple as it should be. With savings accounts, it’s important that you set a goal to let your money grow. As implied by the account type, savings accounts are intended for saving, not for regular transactions. In fact, excessive debits on a savings account could cause you to incur some significant fees, and it’s important that this is understood before choosing this type of account.

When searching for the right savings account, there are a couple things worth thinking through. Savings account fee waivers can be determined by balance thresholds, relationship pricing or customer demographics. Since excessive transactions aren’t encouraged, you won’t typically find fee waivers tied to transactions on savings accounts. Apart from pricing, the other thing to pay close attention to is the interest plan structure, which commonly comes in one of three ways:

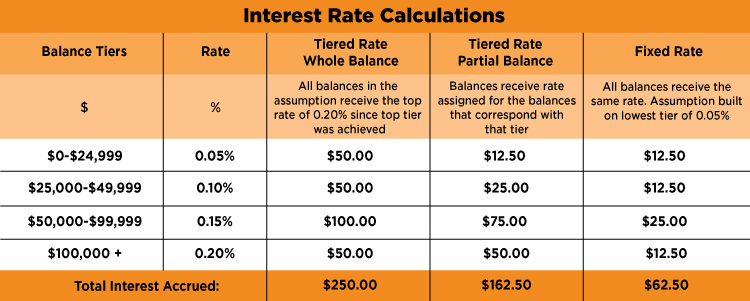

- Fixed rate: A fixed rate savings account is the simplest option and is going to pay the same interest rate on all the funds in the account, regardless of balance. These types of accounts generally require a smaller opening deposit or balance requirement and will typically pay the least amount of interest.

- Tiered rate – whole balance: These accounts are designed for larger balances and are the most rewarding as they’ll pay you the highest rate of interest you’ve earned, based on your tier, for your entire balance. They will likely have a larger opening deposit expectation and a higher balance requirement; however, if you can meet the higher thresholds of the top tiers, you’ll receive a better interest rate.

- Tiered rate – partial balance: Also a tiered interest plan, a partial balance account pays a different interest rate for each tier of the balance. This means that different portions of your money accrue different interest rates rather than one rate for the entire balance. While these accounts have comparable opening deposit expectations and balance requirements as the whole balance method, they ultimately pay out less interest to a comparable interest plan in the whole balance structure.

See illustrative example below, assuming $125,000 in balances held for one year:

Before deciding on a savings account, you should understand the best usage of your money. A savings account may not be the best option once you’ve obtained certain balance levels. What you need to think about is how liquid you need your funds, once they’ve met a certain threshold. If it’s not necessary to have immediate access to excess funds, you may consider a time-deposit account such as a Certificate of Deposit (CD) or Individual Retirement Account (IRA) instead.

If you’re ready to learn more, talk to your banker about the best options for your needs. Browse other Personal Finances articles or contact me to learn more.

Equal Housing Lender. SBA Preferred Lender. NMLS #440379

Equal Housing Lender. SBA Preferred Lender. NMLS #440379