In the last 10 to 15 years, the general public has become increasingly aware of how investment professionals make decisions for their customers and how they are compensated. This positive development has led many to advocate for investment professionals to adhere to a “Fiduciary Standard.”

What is a fiduciary?

In the investment world, an advisor who works on a fiduciary basis charges a fee (usually a percentage of the portfolio) for managing client assets. They do not receive commission for recommending any one investment over the other. They are paid for their advice, and they are required to make recommendations that put clients’ interests ahead of their own.

What is the “Fiduciary Standard,” and why is it important?

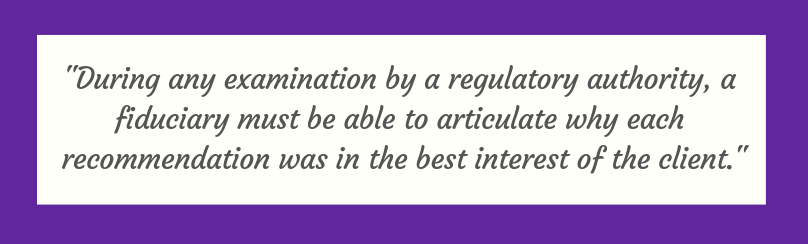

During any examination by a regulatory authority, a fiduciary must be able to articulate why each recommendation was in the best interest of the client and that proper due diligence of each recommendation was done. Fiduciaries are held to a higher standard than the traditional commission based model, which requires that investments are “suitable” for customers.

In the past, there have been cases of the traditional commission model creating “conflicts of interests” where the investment professionals have recommended products that offer additional incentives like trips or higher commissions that the consumer was not aware of at the time of the purchase. This has led some to argue for a “fiduciary for all” standard in the investment world.

Is working with a fiduciary right for you?

I am a strong advocate for acting in the best interest of clients, and I believe every investment professional must be committed to doing the same. Rules that limit excessive commissions and incentives like trips should be in place to help protect the general public. In my practice, I strongly promote accounts that charge a fee for managing assets (a fiduciary model) rather than getting paid on commission for selling a product. However, there are instances in which a investment professional can use the traditional commission-based model and it is best for the client. It’s important to discuss both options with your advisor to determine which model is a better fit for you.

Keep in mind, the fiduciary model is just one part of what you should look for in an investment provider. When evaluating an investment professional, you need to consider their knowledge, their understanding of your personal financial situation and goals, and the reasoning for their recommendations in addition to how they are paid.

In many cases, the fiduciary model provides the best solutions for the client and ensures the financial professional is held to a high standard. I am a strong believer in this model, and I believe it’s a conversation you should have with your investment professional.

Jason Egge is a registered representative with Securities America, Inc. Securities offered through Securities America, Inc., member FINRA/SIPC. Advisory services offered through Securities America Advisors, Inc. Bankers Trust, BTC Financial Services, a division of Bankers Trust, and Securities America are separate companies. Securities America and its representatives do not provide tax advice; it is important to coordinate with your tax advisor regarding your specific situation. Not FDIC Insured. No Bank Guarantees. May Lose Value. Not a Deposit. Not Insured by Any Government Agency.

Equal Housing Lender. SBA Preferred Lender. NMLS #440379

Equal Housing Lender. SBA Preferred Lender. NMLS #440379